Life insurance that protects you

at every stage of life.

An Indexed Universal Life policy is the only financial tool designed to work in three directions at once — protecting your income, your family, and your retirement.

— Kirt Patel, Licensed Insurance Broker

Why Families Choose Us

Free Personalized IUL Review

Build a personalized IUL strategy for your family, retirement, and future.

In just a minute, tell me a little about yourself. I'll personally review your financial goals, budget, current coverage, and whether an Indexed Universal Life policy is the right fit for your situation. If another option makes more sense, I'll tell you that too.

↓ Continue Reading Below

What My Clients Are Saying

Real reviews from real clients

"Mr Kirt Patel treated me with kindness and got me the best deal he could on my life insurance. I am forever grateful because I don’t know a lot on this subject. He took his time and explained things and did not pressure me into buying anything. I believe that is one of the things I liked about him. I do not like being pressured. Thank you again Mr Patel"

"My name is Lisa and I am from Boston, MA. Just wanted to share my experience with everyone on how grateful I am to have had the honor of allowing Kirt Patel to guide me through the kind of life insurance I was able to receive … and let me tell you not only was he pleasant very professional patient and kind, he also became a friend after our many conversations… I would recommend anyone in the need of life insurance, reach out to Kirt he will absolutely take very good care of you and that is my advice!!"

"For anyone that is considering getting life insurance, Kirt Patel is definitely the guy you want to do business with. I really just didn't want to think about dying. However, death is inevitable. I am on a very limited income and wasn't even sure I could afford enough coverage. Kirt found a policy that I can afford. And made me smile and even laugh while doing it! I highly recommend giving Kirt Patel a call."

Is Indexed Universal Life Right for You?

IUL can be an excellent fit if you're looking for more than just life insurance.

While no single policy is right for everyone, Indexed Universal Life is often a strong choice for people who want lifelong protection combined with long-term financial flexibility.

Families

Protect loved ones while creating financial flexibility for the future.

Business Owners

Create tax-advantaged assets while protecting your family and business.

Retirement Planners

Looking for another tax-advantaged retirement income strategy.

Income Protectors

Want living benefits in case a serious illness affects your ability to earn an income.

Why Families Choose IUL

One policy. Three powerful benefits.

Unlike many life insurance policies that focus on a single purpose, an Indexed Universal Life policy can help protect your family today while creating financial flexibility for the future.

Protect the people you love.

Your beneficiaries can receive an income tax-free death benefit that helps protect your family's financial future.

- Replace lost income

- Help pay off debts or a mortgage

- Cover education expenses

- Leave a financial legacy

Build long-term financial flexibility.

Part of your premium builds cash value that grows tax-deferred based on index performance, subject to policy terms.

- Tax-deferred growth potential

- Access through policy loans

- Supplement retirement income

- Maintain lifelong coverage

Protection while you're living.

Many IUL policies include accelerated death benefit riders that may provide access to a portion of your death benefit if you experience a qualifying illness.

- Chronic illness protection

- Critical illness protection

- Terminal illness protection

- Greater financial peace of mind

Is an IUL Right for You?

Like any financial strategy, Indexed Universal Life isn't the right solution for everyone.

My job isn't to sell you an IUL—it's to help you determine whether it actually fits your goals. If another type of life insurance makes more sense, I'll tell you that too.

✅ An IUL May Be a Great Fit If You...

- Want permanent life insurance that lasts your lifetime.

- Would like the opportunity to build tax-advantaged cash value over time.

- Want living benefits that may help during certain serious illnesses.

- Are planning for retirement and want another source of potential tax-advantaged income.

- Want flexibility to adjust your coverage as life changes.

❌ Another Policy May Be Better If You...

- Only need inexpensive temporary life insurance for a short period.

- Are looking for a short-term investment rather than long-term protection.

- Need the absolute lowest monthly premium possible.

- Don't want to actively fund a policy over time.

- Simply want basic life insurance without any additional features.

Every family's situation is different. During your complimentary review, I'll explain your options and recommend the solution that best fits your goals—even if it isn't an Indexed Universal Life policy.

How It Works

What makes an IUL different from anything else.

An Indexed Universal Life policy combines permanent life insurance with a cash value component tied to a market index — but with a critical difference most investments don't offer.

Indexed to market growth — without the risk

Your cash value grows based on the performance of a stock market index like the S&P 500. When the market goes up, your account is credited with gains. When the market goes down, your account is protected by a floor — typically 0% — meaning you never lose the value you've already built.

Tax-deferred growth inside the policy

Unlike a brokerage account or 401k, the growth inside your IUL is tax-deferred. Your cash value compounds without being reduced by annual taxes on gains. Over decades, this difference is enormous.

Be your own bank — tax-free access through policy loans

This is what people mean when they talk about "infinite banking" or "being your own bank." When you're ready to access your cash value — for a business opportunity, college tuition, or retirement income — you take loans from the policy. These loans are generally not taxable income. You pay yourself back instead of a bank, and your cash value keeps growing as if the loan was never taken.

Increasing death benefit option

As your cash value grows, your total death benefit grows with it. Your policy becomes more valuable — not less — the longer you hold it.

Premium flexibility

Unlike whole life insurance, an IUL lets you adjust your premiums within limits as your life changes. You're not locked into a rigid payment forever — giving you flexibility if your income or priorities shift over time.

The lowest cost permanent coverage available

Term insurance is cheap but temporary — when it expires, you have nothing. Whole life is permanent but expensive. An IUL gives you permanent coverage with cash value growth at a significantly lower cost than whole life, while offering features whole life can't match.

Compare Your Options

Which policy best fits your goals?

Every type of life insurance has strengths. The right choice depends on what you're trying to accomplish. Here's a quick comparison to help you understand the differences.

👉 Swipe left to compare all coverage options

| Feature | Term Life | Whole Life | IUL |

|---|---|---|---|

| Family Protection | ✔ Included | ✔ Included | ✔ Included |

| Lowest Cost | ✔ Best Option | ✖ Highest Cost | ◐ Moderate Cost |

| Cash Value Growth | ✖ No | ✔ Guaranteed | ✔ Growth Potential |

| Retirement Protection | ✖ No | ◐ Can Help | ✔ Designed For This |

| Market Protection | ✖ No | ✔ Stable Growth | ✔ 0% Floor |

| Living Benefits | ◐ Optional Riders | ✔ Often Included | ✔ Often Included |

| Flexible Coverage | ✖ Limited | ✖ Fixed | ✔ Most Flexible |

| Often Best For... | Families needing affordable temporary protection such as for a mortgage. | People who prioritize guarantees and predictable growth. | Families looking for lifelong protection, tax-advantaged cash value growth, and greater financial flexibility. |

Family Protection

Lowest Monthly Cost

Cash Value Growth

Retirement Protection

Market Protection

Living Benefits

Flexible Coverage

Often Best For...

Remember: the best policy isn't the one with the most features—it's the one that best fits your family's goals, budget, and long-term plans.

During your complimentary review, I'll explain the pros and cons of each option and recommend the solution that's best for you—even if it isn't an Indexed Universal Life policy.

Important to Know

Not everyone qualifies — and that's a good thing.

IUL requires an application and health review before approval.

Unlike some basic insurance products, an IUL is a premium financial tool — and carriers want to make sure it's the right fit. Before we submit anything, I will assess your situation, explain exactly what to expect, and make sure you're going into the process with full clarity.

If you don't qualify for an IUL, that's not the end of the road. I will find you the next best alternative — whether that's a different policy structure or a whole life plan that still builds cash value and provides permanent coverage. The goal is always to find what actually works for your life.

The Key Advantage

Market upside. Zero downside.

This is the feature that separates an IUL from nearly every other financial product on the market — and it's why high-income earners increasingly use it as a cornerstone of their financial plan.

0% Floor — You Never Lose

If the index drops 30% in a bad year, your cash value is credited 0% — not negative. Your principal is always protected.

Participation in Index Gains

When markets perform well, your cash value is credited a portion of those gains — up to the policy's cap rate.

Gains Lock In Annually

At the end of each crediting period, your gains are locked in permanently. Future market drops cannot take back what you've already earned.

No Market Volatility Anxiety

You don't have to watch the market daily or worry about your retirement disappearing in a correction. Your floor protects your future.

Built Around Your Goals

Your IUL is structured for what matters most to you.

There's no one-size-fits-all IUL. I structure each policy specifically around your primary objective — whether that's maximizing what you leave behind or maximizing the income you can access in retirement.

🛡️ Maximum Death Benefit

Ideal if your primary goal is leaving the largest possible tax-free inheritance for your family or business partners. The policy is structured to maximize the face amount relative to your premium.

- Higher death benefit from day one

- Still builds cash value over time

- Includes living benefits for illness

- Increasing death benefit option available

- Best for: family protection, estate planning, business buy-sell agreements

💰 Maximum Cash Value (LIRP)

Ideal if your primary goal is building tax-advantaged wealth you can access in retirement — sometimes called a Life Insurance Retirement Plan (LIRP). The policy is overfunded to maximize cash value accumulation, giving you the most money to borrow from tax-free.

- Faster cash value growth

- More money available for tax-free loans

- Supplemental retirement income stream

- Includes living benefits for illness

- Best for: retirement planning, high-income earners, maxing tax-advantaged accounts

Is This For You?

An IUL makes sense if…

You want life insurance that also builds wealth over time — not just a death benefit

You're maxing out your 401k and IRA and looking for additional tax-advantaged savings

You're worried about running out of money in retirement and want a tax-free income stream

You've heard about "being your own bank" or infinite banking and want to understand if it's right for you

You want market participation without the risk of losing what you've saved

You're between ages 18–65 and want to lock in permanent coverage while you're healthy

You've researched IUL or LIRP strategies and are ready to talk to someone who can actually execute it

You're a business owner looking for a tax-efficient way to protect yourself or fund a buy-sell agreement

Why Timing Matters

Every year you wait costs you twice.

This is the part most people don't realize until it's too late. An IUL isn't just age-sensitive — it's compounding-sensitive. The earlier you start, the more powerful it becomes.

Your premium goes up every year you wait

IUL premiums are based on your age at the time of application. The older you are, the higher your cost of insurance inside the policy — and the more of your premium goes toward coverage instead of cash value. Locking in now locks in your current age and health rating permanently.

Compounding loses its power the longer you delay

The biggest driver of cash value growth in an IUL is time — not the amount you put in. A policy started at 35 will dramatically outperform one started at 45, even with identical premiums. Every year of compounding you miss is a year you can never get back.

Health changes can affect your eligibility

You qualify today based on your current health. A diagnosis, a new medication, or a change in health status can affect the terms you're offered — or your ability to qualify at all. The best time to apply is while you're at your healthiest.

Your retirement runway is shortening every year

An IUL needs 10–20 years to build meaningful cash value. If you're planning to retire in 15 years and start today, you have just enough runway. If you wait 5 more years, you may not have enough compounding time to make it work the way you envision.

Why Families Choose Generis

Personalized guidance. Multiple insurance companies. One trusted advisor.

Buying life insurance shouldn't feel confusing or high-pressure. As an independent broker, I work for you—not the insurance company. My goal is to help you understand your options and recommend the policy that best fits your family's goals.

Independent Broker

I compare multiple insurance companies so you're never limited to one carrier's products or pricing.

A-Rated Insurance Companies

I partner with financially strong carriers that have a long history of paying claims and protecting families.

Personalized Recommendations

Every recommendation is based on your goals, health, budget, and long-term financial plans—not a sales quota.

You'll Work Directly With Me

No call centers. No rotating agents. You'll always have one licensed advisor who knows your situation.

Support Beyond Your Policy

I'm here long after your policy is issued, whether you need a review, beneficiary updates, or help filing a claim.

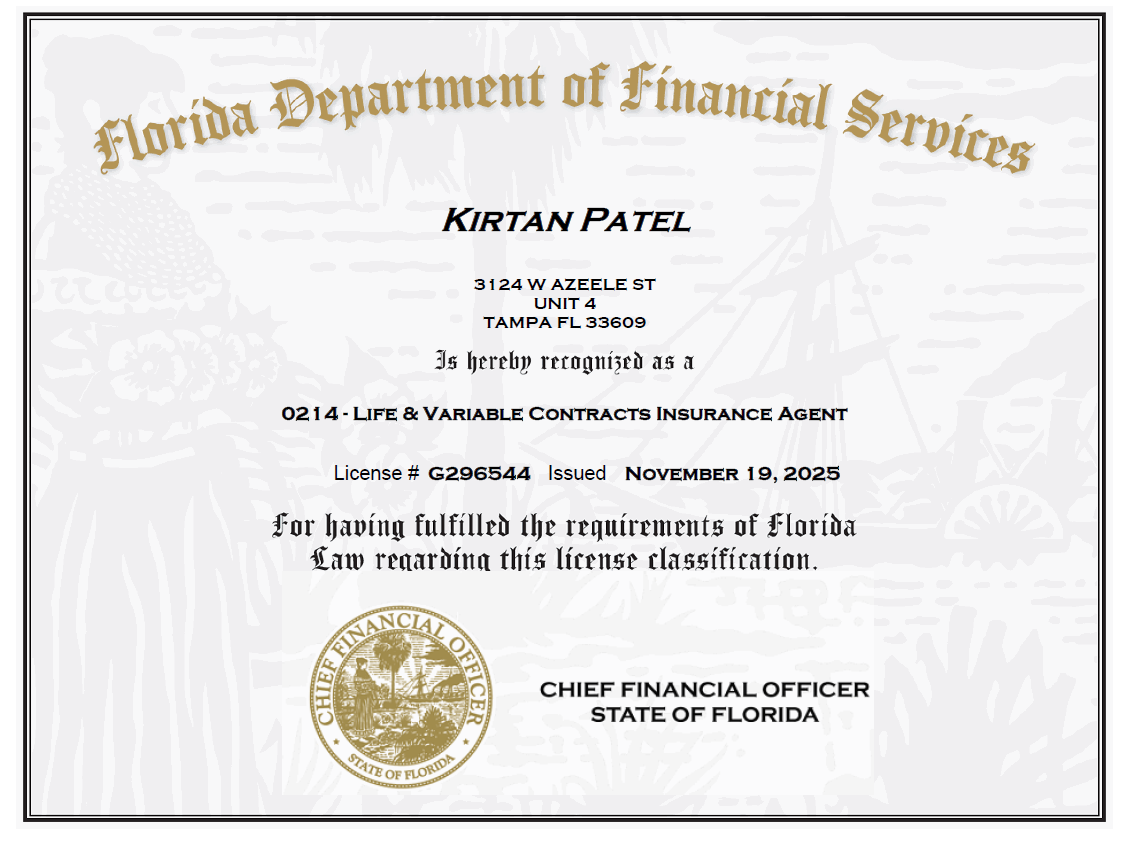

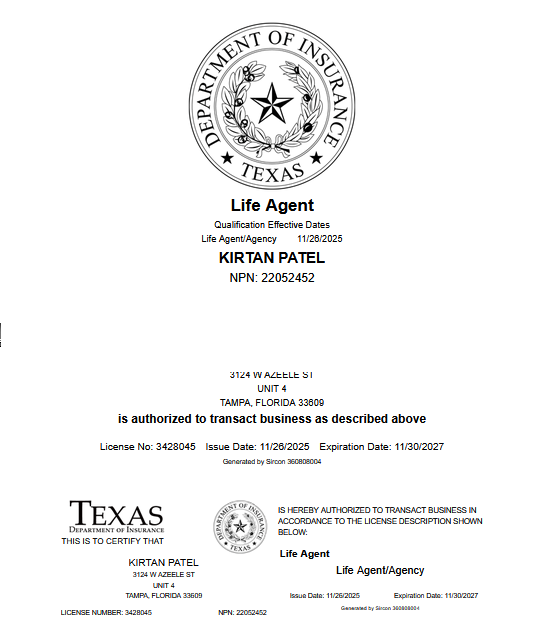

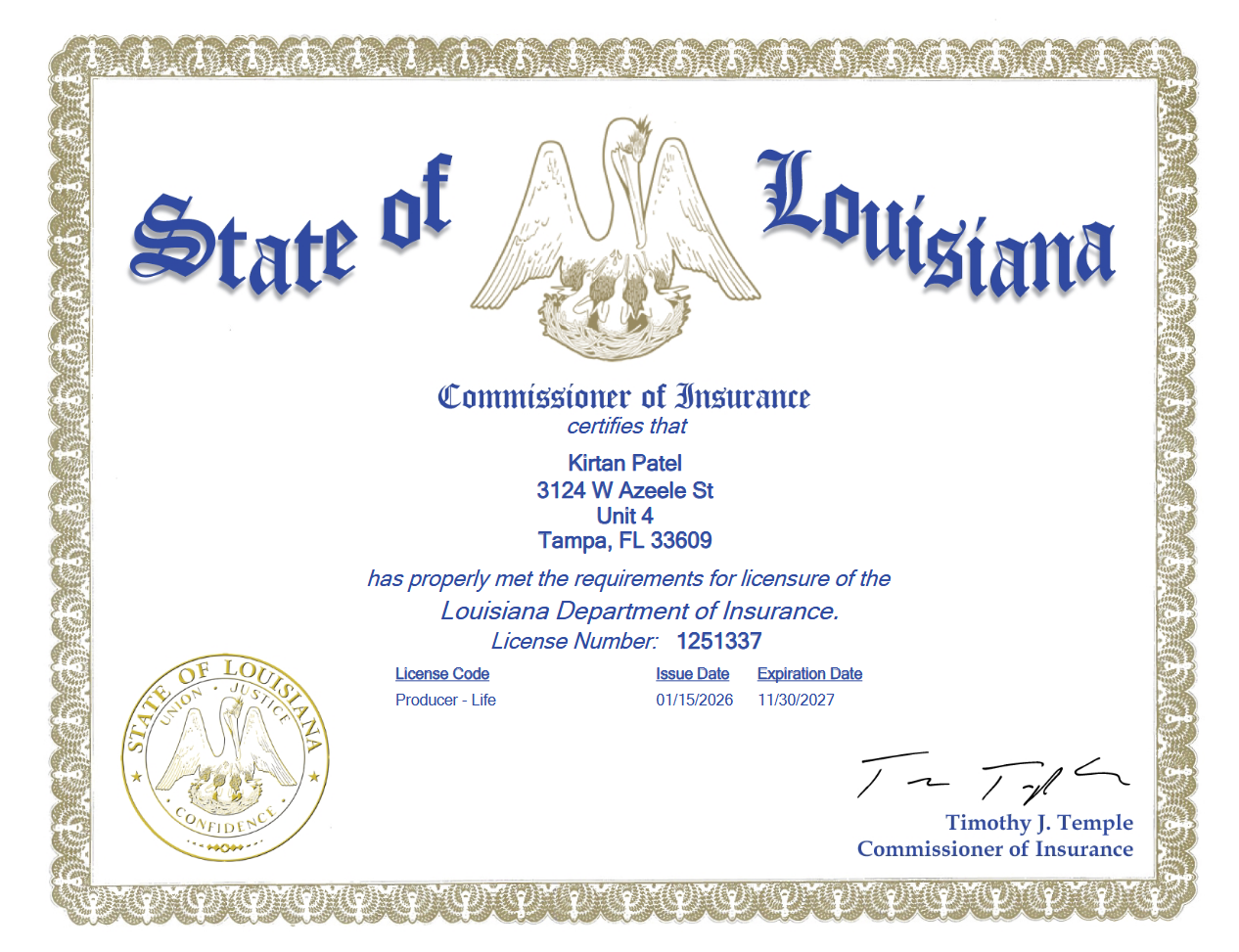

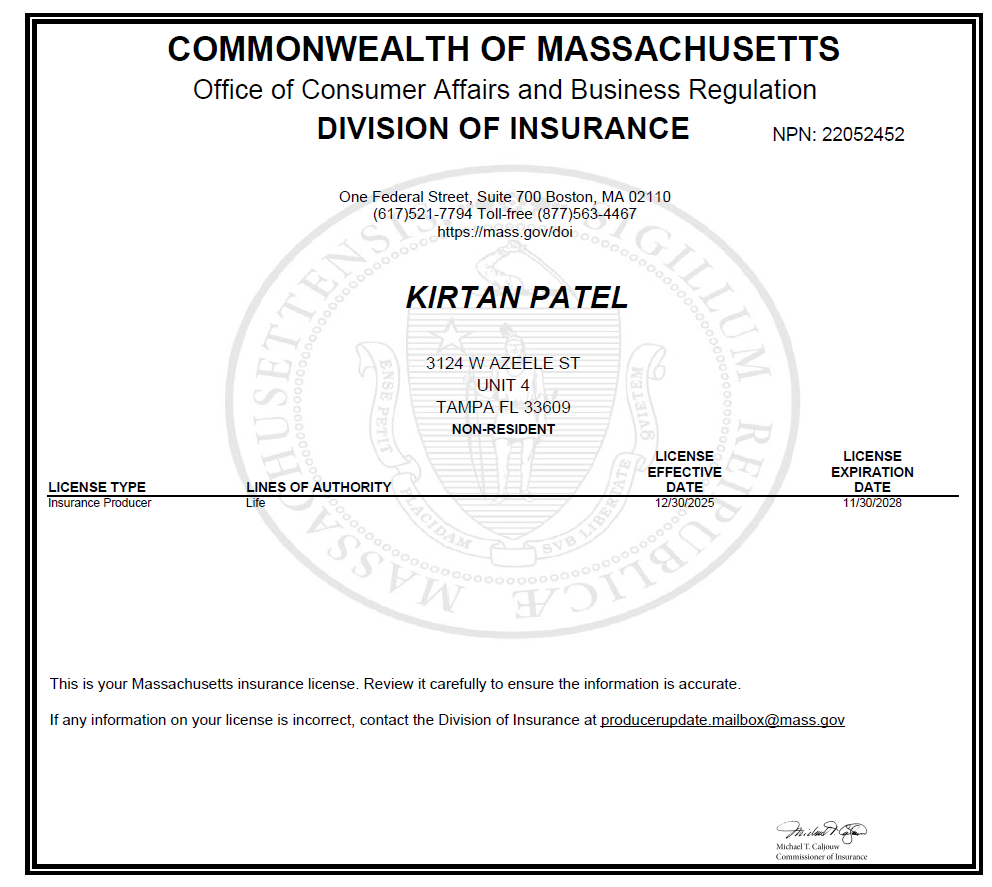

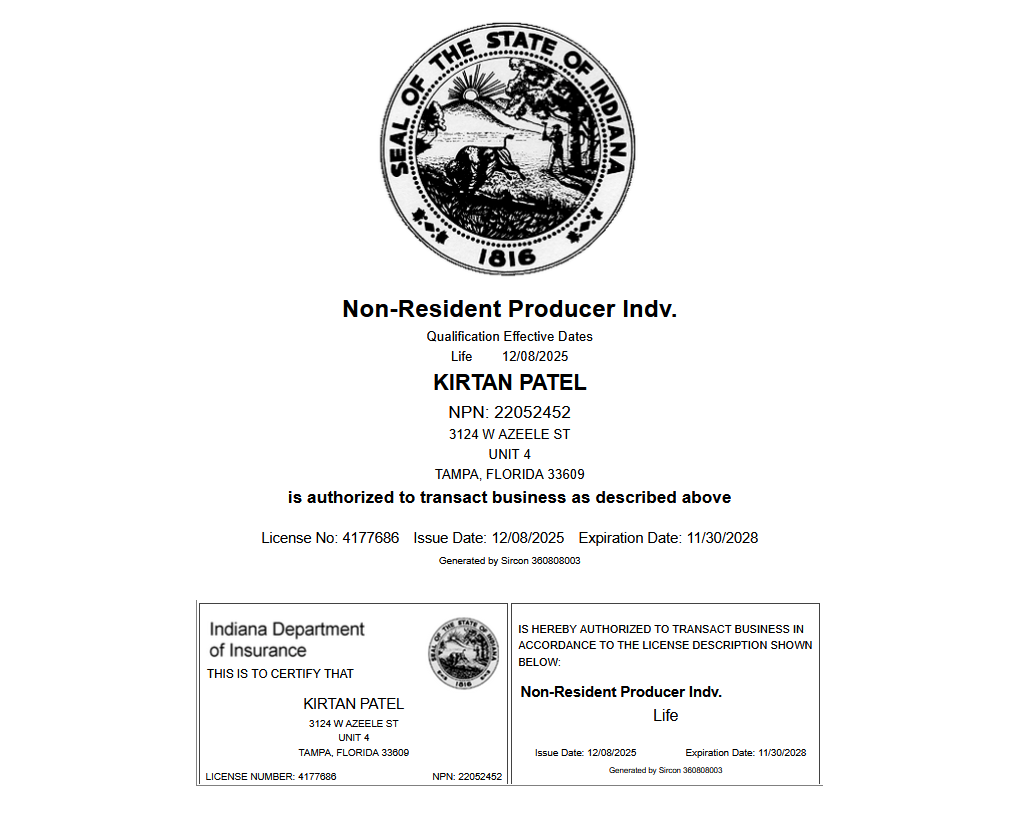

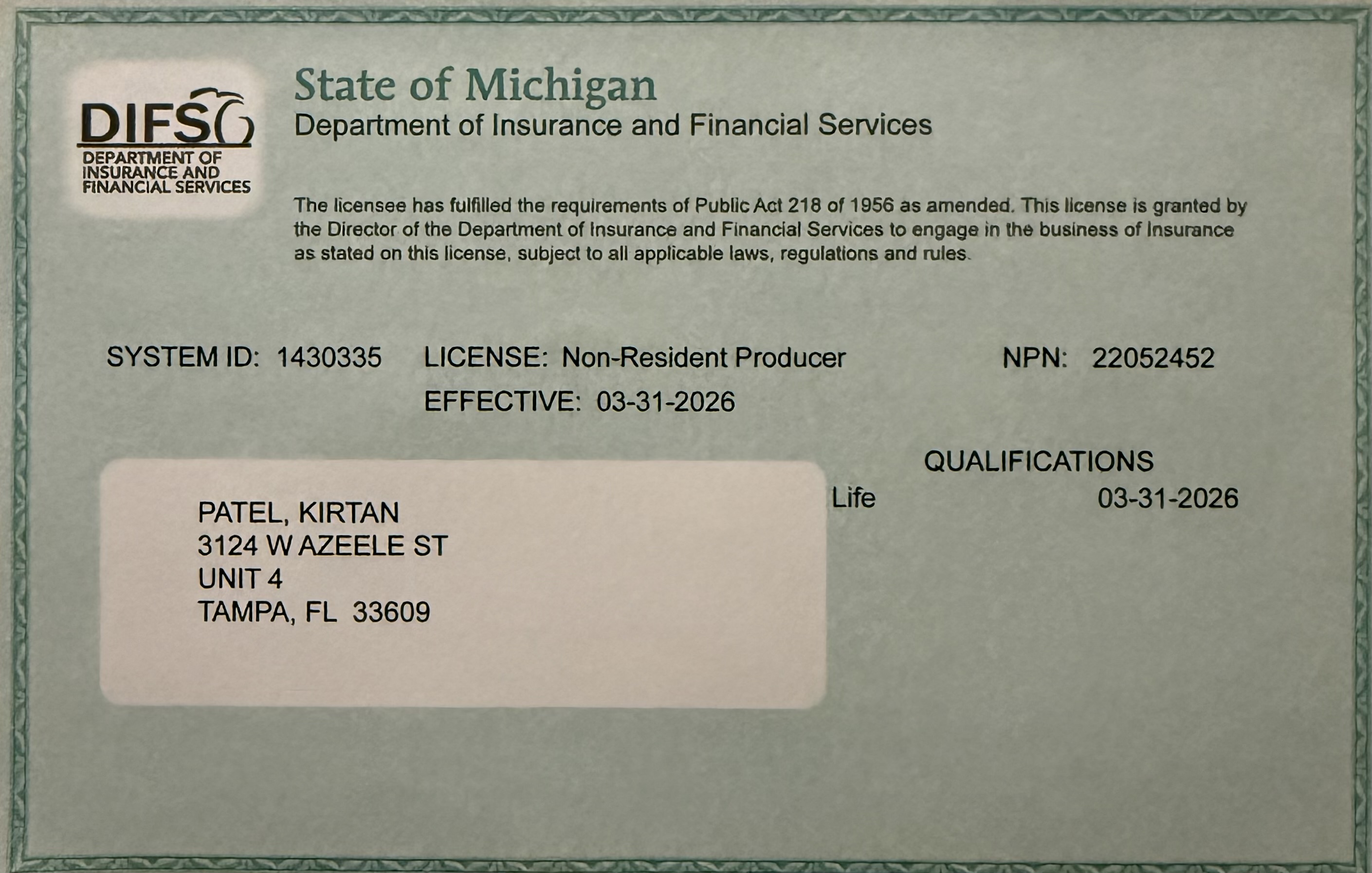

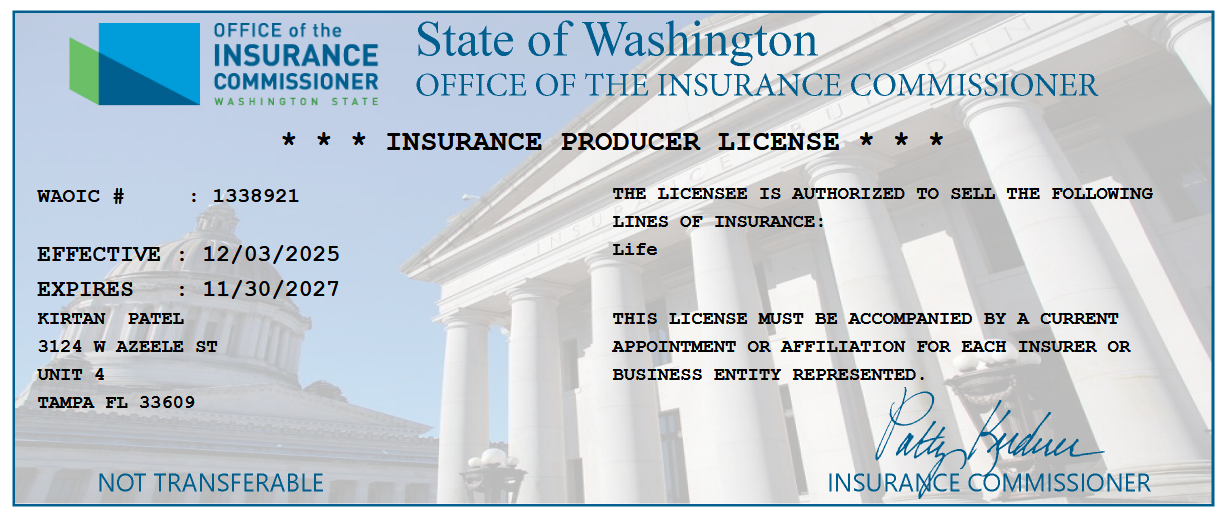

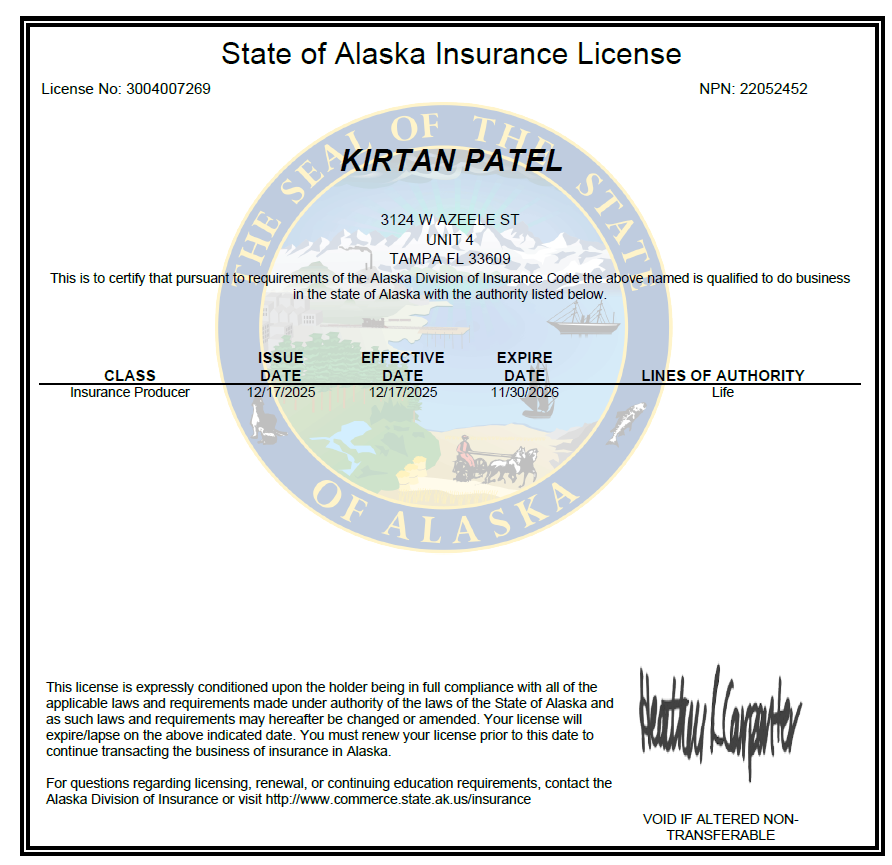

Licensed in 9 States

Families across nine states trust Generis Organization for honest guidance and long-term protection.

The Process

Simple. Personalized. No pressure.

Getting an IUL structured correctly takes a real conversation — not a one-size-fits-all quote. Here's exactly what happens when you reach out.

You Request a Free Review

Fill out the form. Tell me your goals — death benefit, wealth building, retirement income, or all three. Takes less than 2 minutes to complete.

I Design Your Illustration

I shop Transamerica, American Amicable, and F&G to build a personalized illustration tailored to your age, budget, and goals — showing you exactly how the policy performs over time with realistic numbers.

You Make an Informed Decision

No pressure. I walk you through every number clearly and honestly. If you want to move forward, he submits your application. If not, there's zero obligation.

Common Questions

Answers before you reach out

Meet Kirt Patel

Helping Families Protect What Matters Most

Founder of Generis Organization • Independent Life Insurance Broker

I believe life insurance should never feel confusing or high-pressure. My job is to help you understand your options, answer your questions honestly, and recommend coverage that fits your family's goals—not someone else's sales target.

As an independent broker, I compare multiple highly rated insurance companies so you're not limited to one carrier's products. Every recommendation is personalized to your goals, health, budget, and your family's needs.

My relationship with clients doesn't end once a policy is issued. Whether you need to review your coverage years later, update beneficiaries after a life change, or your family ever needs help filing a claim, I'll be here to guide you every step of the way.

My goal is simple: to give every individual and family confidence that the people they love—and the life they've worked so hard for—are protected.

Compare Coverage From Trusted Insurance Companies

Transparency & Licensing

Licensed to Serve Families Across 9 States

Every license below can be viewed in full because I believe transparency builds trust. Click any license to verify my credentials.

Personalized IUL Review

Let's tailor your IUL to you and your family.

A few quick questions so I can prepare real recommendations before we talk. Takes less than 2 minutes to complete.

Explore More

Personalized illustration · No pressure